Property Investment risks. Here are 5 of them.

All investments come with risk(s). That includes even Fixed Deposits! The risk of not having enough and realizing it only 30 years later. Imagine… we save every cent we have every month ONLY into Fixed Deposits and realized 30 years later that the 1.8% interest rate per year is actually lower than even the officially announced inflation rate which is usually between 3 – 3.5 percent? What happens when we discover this only after we retire and income has stopped and we see a dropping number in our account every month? Today, let’s just look at 5 risks for property investments.

#1 Mistakes are costly; money and time

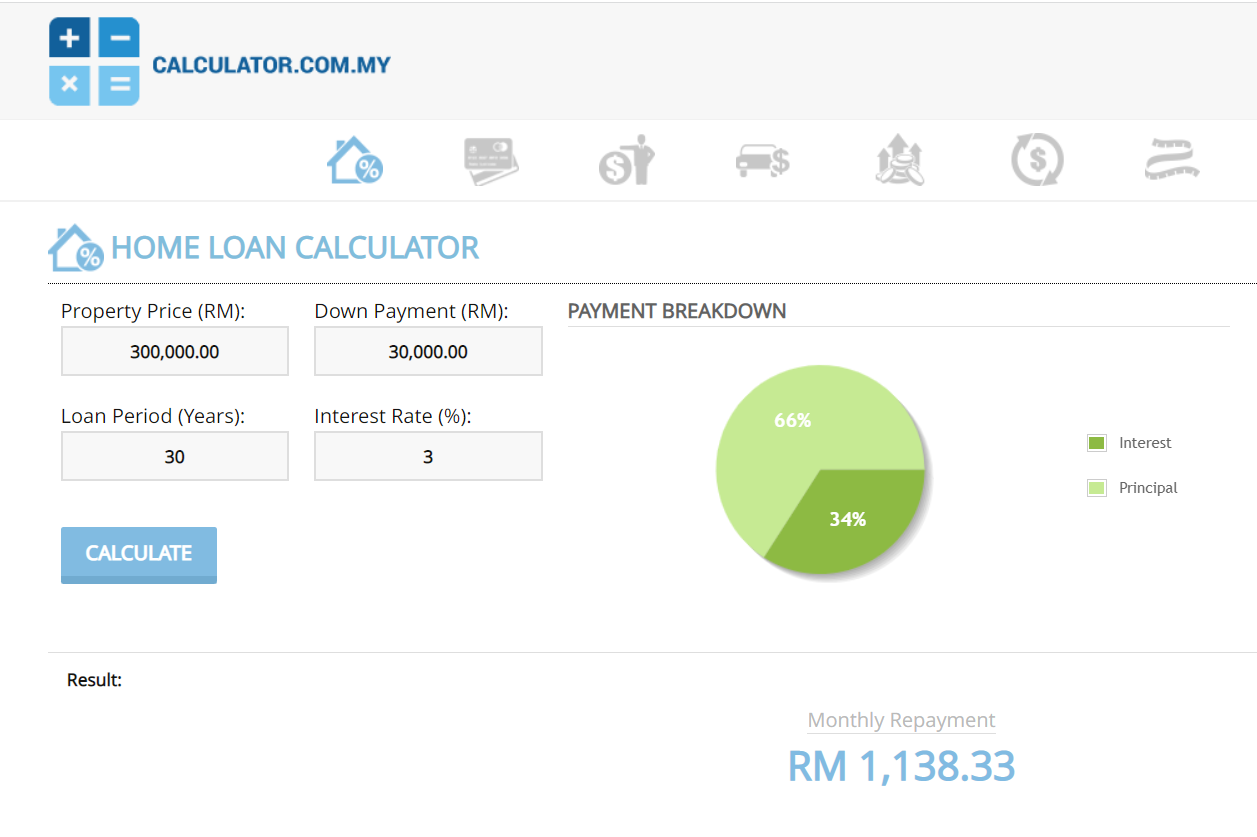

When it come to a property, it’s really quite dangerous. Imagine buying an affordable home of RM300,000 and then realized we totally hate the place? Well, it’s RM1,140 per month for the next 360 months and by the end, the total amount paid is very lose to RM410,000 (after including interest) even though our loan from the bank was for RM270,000? We are only talking about a RM300,000 home for this case.

As we needed to pay this RM1,140 per month and not staying / unable to stay there and on top of this still have to pay rental, it will be very financially stressful. We will need to earn by far more money and save it up in order to buy another place which we like maybe many years in the future. This is why we will lose both money and time. Do enough due diligence to minimise this risk.

#2 Unforeseen circumstances hard to predict (does not need to be a financial crisis)

Many years ago, my good friend Mr. C told me that an owner arrogantly rejected a RM1.2 million offer for a semi-detached home and said that there was a unit within the same row which sold for RM1.6 million. My friend pointed out to him that the RM1.6 million unit was bigger. Under normal circumstances, the buyer could wait and get the price he wanted.

Then, Penang was hit by a flash flood in 2016. That whole row of semi-detached homes were all under 60cm of water and the road in front of the row of homes cracked as well. The buyer called my good friend and says that he is now willing to consider RM1.2 million. My friend politely informed him that he could only try and market to more people but the photos of the homes under water has gone viral earlier…

#3 Hard to run (cut loss) or sell (quick profit) if ever needed

If we have money invested in the stock market and we pay very close attention, if the company share suddenly show a sharp correction, it will be possible to cut loss and just sell all the shares and take back the money within days. If the shares suddenly spiked upwards, we could also sell and have the money in our bank account in a few days.

Now imagine the property price suddenly dropping because a recession starts. In order to sell, we need to make sure we appoint a good real estate agent, the person needs time to post up the advertisement and the potential buyers need to have time to come and view the property. After viewing, the buyer will need time to decide and perhaps even a few other viewings in order to compare objectively. Even after the confirmation, the money from the property from the bank will only be in the owner’s account many weeks later. This is the fastest.

Assuming, the prices suddenly spiked. The same thing would happen too because selling will also be taking a long time! Property is an illiquid asset.

#4 What if the tenant came from Hxxx?

Just google for ‘bad tenants’ and click on images and start feeling very bad to become a landlord. An image below for reference. Searched on 2nd Jan 2022.

Yes, earning rental yield may not be as straight forward as it seems right. Chasing for rental every month will be very tiring… Evicting a tenant who refused to pay will also be a big hassle too… Let’s not forget the fact that the cost of cleaning up, of repairing all that’s damaged and replacing the items in the home after the tenant has moved out will be another huge financial stress too. Here are some tips on how to choose a good tenant to minimise risk. No such thing as zero risk by the way.

#5 NOT owning even a single property

We save this best one for last. What happens if we did not start our property investment journey at all? Briefly, we believe renting is better than buying? As per advocated by many personal finance experts who said property investment can be easily replaced with stock investment?

The risk is the never-ending rental month after month and year after year until the day we say good bye to the world. Imagine RM1,500 rental per month for just 20 years? RM1,500 x 12 (months) x 20 (years) = RM360,000. Just need to note that this RM360,000 calculation assumes rental does not increase (which is impossible) and that the tenant will always find a good landlord versus a landlord from hxxx.

Conclusion

Here are 5 risks of property investment and the last one is of not having a single property at all which belongs to us. Remember, the essence of investment is so that our investments can grow enough so that we have enough to spend when our income stops.

At the same time, a property investment is also to stop us from paying non stop when our income stops (one day it will). So, reducing the expenses is an extremely important factor as well, not just the building up of wealth. All the best in your property investment journey and remember, if we are able to build wealth way faster in any other type of investment, then perhaps property investment is no longer necessary. Cheers.

Property News Malaysia? Sign up for daily investment news updates (FREE since Nov 2013 and FOREVER). Alternatively, Follow me on Telegram here.

Please LIKE kopiandproperty.my FB page to get daily updates about the property market beyond kopiandproperty.my articles. Else, follow me on Twitter here.

Next suggested article: Property price expected to rise

Leave a Reply